First-Time Home Buyer Washington State: Complete 2025 Guide and Programs

First-Time Home Buyer Programs in Washington State 2025

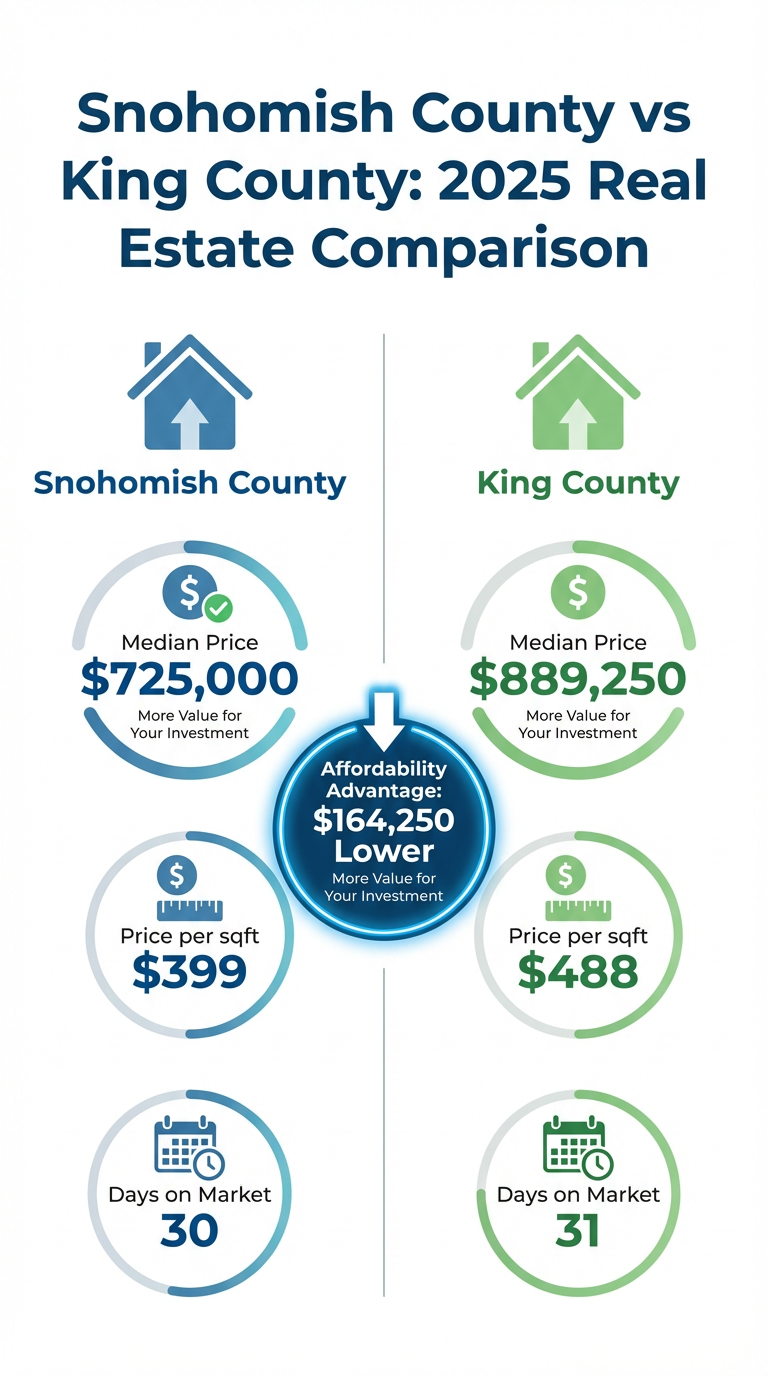

Breaking into Washington State's real estate market as a first-time home buyer can feel overwhelming, especially with King County's median price at $889,250 and Snohomish County at $725,000. However, Washington offers some of the most generous first-time buyer programs in the nation, with assistance ranging from $10,000 to $90,000 depending on location and eligibility.

This comprehensive guide walks you through every program, requirement, and strategy for successfully purchasing your first home in Washington State in 2025.

Washington State Housing Finance Commission Programs

The Washington State Housing Finance Commission (WSHFC) provides the primary first-time buyer programs in the state. The average homebuyer receives $10,000 in down payment assistance from WSHFC, with some programs offering significantly more.

Home Advantage Program

The Home Advantage program offers reduced interest rates and down payment assistance with the following features: down payment assistance up to 4-5% of loan amount, minimum credit score of 620, maximum debt-to-income ratio of 50%, annual income limit under $180,000, compatibility with FHA, VA, USDA, and conforming loans, and eligibility that extends to repeat homebuyers.

The program provides competitive interest rates below market averages and can be combined with various loan types. Eligible properties include single-family units, townhomes, condominiums, and manufactured homes.

House Key Opportunity Program

Designed for homebuyers with lower incomes, this program features income thresholds from $100,000 to $175,000 (varies by location and household size), home purchase price limits from $345,000 to $750,000 (depending on location), minimum credit score requirement of 620, competitive interest rates particularly for FHA, VA, and USDA loans, and a special interest rate discount for conventional loans if income is below 80% of area median income.

Down Payment Assistance Programs

Home Advantage DPA: Provides up to 4% of total mortgage amount (5% for HFA Preferred loans) as a no-interest loan with deferred payments for 30 years. Special programs exist for high-cost areas, offering up to $55,000 in Seattle. Repayment is required upon sale, refinance, or full mortgage repayment.

Home Advantage DPA Needs Based: A second mortgage loan with 1% interest rate and 30-year deferred payments, providing up to $10,000 for down payment needs. Income limits are $115,900 ($147,400 in King or Snohomish counties).

Opportunity DPA: A second mortgage of up to $15,000 with 1% interest rate and 30-year deferred payments, paired with the House Key Opportunity first mortgage. Lower income restrictions apply based on household size and location.

Veterans DPA: Eligible veterans can receive up to $10,000 in down payment assistance as a second mortgage with 30-year deferred payments at 3% interest. Can be combined with either Home Advantage or House Key Opportunity.

HomeChoice Disability DPA: Provides up to $15,000 if applicant or household member has a disability, structured as a second mortgage with 30-year deferred payments at 1% interest.

City-Specific Down Payment Assistance

Seattle

The City of Seattle's Office of Housing offers exceptional assistance for low-income first-time buyers with maximum assistance up to $90,000 for homes with 3+ bedrooms, standard assistance up to $70,000 for homes with fewer bedrooms, and a loan cap of $55,000 for certain loan types. Eligibility is limited to low-income first-time buyers.

Tacoma

The City of Tacoma's DPA program provides maximum assistance up to $60,000 as a no-interest, 25-year loan. Income must be at or below 80% of area median income, and applicants must complete the WSHFC homebuyer course.

Federal Loan Programs for First-Time Buyers

FHA Loans

Federal Housing Administration loans are popular among first-time buyers, requiring minimum down payment of 3.5% for FICO scores 580+ (10% for scores 500-579). Current rates range from 5.875% to 5.99% as of December 2025. The 2025 loan limits are $524,225 for single units to $1,008,300 for four-unit properties (higher in high-cost areas). Maximum DTI is up to 57%, and mortgage insurance is required (upfront fee plus annual premiums).

For a $725,000 home in Snohomish County, 3.5% down would be $25,375—significantly more accessible than the traditional 20% ($145,000).

VA Loans

For eligible veterans, active-duty service members, reservists, and surviving spouses, VA loans offer zero down payment, current rates of 5.99% to 6.0%, minimum credit score often 620 (varies by lender), no mortgage insurance after closing, lower interest rates than most other mortgages, and require a Certificate of Eligibility from the VA.

USDA Loans

For low-to-moderate income individuals buying in designated rural areas, USDA loans provide zero down payment, credit score requirements that vary by lender (often 640), low mortgage insurance rates compared to FHA, but with geographic restrictions to USDA-eligible rural areas.

Surprisingly, some areas within commuting distance of Seattle tech hubs qualify for USDA loans, making this an option worth exploring for those willing to live in more rural settings.

Conventional 97 Loans

Fannie Mae and Freddie Mac programs require just 3% down ($21,750 on a $725,000 home) with minimum credit score of 620. Mortgage insurance can typically be removed after reaching 20% home equity. Programs like Fannie Mae HomeReady and Freddie Mac Home Possible offer flexible down payment sources.

Getting Pre-Approved: Your First Critical Step

Before touring homes, securing pre-approval is absolutely essential in Washington's competitive market. Pre-approval demonstrates to sellers that you're a serious buyer with verified financing, giving your offer significantly more weight than those from buyers with only pre-qualification letters.

Documents You'll Need

Gather these documents before meeting with lenders: pay stubs from the last 30 days showing year-to-date earnings, W-2 forms from the previous two years, tax returns from the last two years (especially important if you have RSU income or side work), bank statements for two months for all accounts, investment account statements if using stocks, RSUs, or other investments for down payment, credit report authorization (lenders will pull your credit), employment verification letter from HR or recent offer letter, and debt documentation including student loans, car loans, and credit card balances.

How Much Home Can You Afford?

Lenders use debt-to-income (DTI) ratios to determine borrowing capacity. Most conventional loans require DTI below 43%, though some programs allow up to 50%.

For Snohomish County's median price of $725,000 with 20% down payment of $145,000, loan amount of $580,000, monthly P&I at 6.2% of approximately $3,560, property taxes of roughly $550/month, and insurance of about $150/month, total monthly cost is approximately $4,260, requiring an annual income of around $182,000.

However, with 3.5% down (FHA), your down payment drops to $25,375, though monthly payments increase due to mortgage insurance. This makes homeownership accessible to a much broader range of first-time buyers.

The Home Buying Process Timeline

The typical timeline from offer acceptance to closing is 30-45 days. Days 1-3 involve opening escrow and depositing earnest money (1-3% of purchase price). Days 3-10 are for completing home inspection ($400-$600) and negotiating repairs or credits. Days 7-14 cover appraisal ordering and completion ($500-$700). Days 10-21 focus on finalizing mortgage approval and providing additional documentation. Days 28-30 include the final walkthrough to verify condition. Day 30-45 is closing day when you sign documents, transfer funds, and receive keys.

Closing Costs to Expect

Budget for closing costs of 2-5% of the purchase price, including lender fees and origination charges, title insurance and escrow fees, appraisal and inspection fees, recording fees and transfer taxes, prepaid property taxes and insurance, and HOA transfer fees if applicable.

On a $725,000 home, expect $14,500-$36,250 in closing costs. However, many first-time buyer programs offer assistance with these costs, and you can negotiate for seller-paid closing costs in slower market segments.

Building Your Down Payment Strategy

Consider these down payment sources: vested RSUs (many tech professionals use equity compensation, but plan for tax implications), 401(k) loans allowing you to borrow up to $50,000 or 50% of vested balance without penalties for first-time buyers, IRA withdrawals of up to $10,000 penalty-free for first-time home purchase, gift funds from family members with proper documentation, and down payment assistance programs from state and local sources that can contribute thousands.

Why Choose Odigo Club

At Odigo Club, we specialize in helping first-time buyers navigate Washington's real estate market. Our agents understand the complexities of state and local assistance programs, and we work with lenders who are experts in first-time buyer financing.

We provide guidance on all available first-time buyer programs and assistance, connections to lenders experienced with WSHFC and local programs, education on the entire home buying process, negotiation expertise to maximize your purchasing power, and support from pre-approval through closing and beyond.

Ready to start your first-time home buying journey? Contact Odigo Club today to connect with an agent who specializes in helping first-time buyers. With programs offering up to $90,000 in assistance and multiple low-down-payment options, homeownership in Washington State is more accessible than you might think.

About the Author

Peter Kim

Peter Kim is the owner of Odigo Real Estate Club, a leading real estate agency in the Greater Seattle area that specializes in residential, commercial, and luxury properties. With over 10 years of experience and a team of highly skilled agents, Peter brings a wealth of knowledge and expertise to the real estate space.